When facing a job loss, severance pay can provide a financial cushion as you move forward. However, a common question often arises: Is severance pay taxable? Knowing the tax implications of severance payments can help you prepare financially, make smart decisions, and understand options for reducing your tax burden. In this article, we’ll cover the basics of severance pay taxation, options to minimize taxes, and how severance may impact other benefits like unemployment. Additionally, we’ll explore tips shared by others online about severance pay and highlight CuraDebt’s services to help you manage tax debt if you’re facing financial challenges.

Is Severance Pay Taxable?

Yes, both federal and state governments typically consider severance pay taxable income, subject to income tax, Social Security, and Medicare withholding. Since the IRS treats severance pay like ordinary wages, it may push you into a higher tax bracket and increase your tax liability for the year. This can come as a surprise, especially during a time when you’re adjusting to new financial circumstances after a job change.

If you’re wondering how to minimize taxes on your severance pay, keep reading for practical strategies that can help reduce the tax burden and maximize your financial benefits.

How To Minimize Taxes On Severance Pay

Now that we understand that severance pay is taxable, let's explore some strategies to reduce this financial burden.

1. Negotiate the Payment Timing

One strategy is to negotiate the timing of your severance payment. By deferring your payout to a different tax year, you could potentially reduce the tax impact if your income will be lower in the following year. Timing your payout might help reduce your taxable income for one of the years, especially if it will push you into a lower tax bracket.

2. Contribute to a Retirement Account

Contributing to retirement accounts, such as an IRA or 401(k), can lower your taxable income for the year. Some companies allow employees to deposit severance payments into these accounts, reducing the amount of taxable income and helping you save for the future.

3. Consider a Lump-Sum Payment

While a lump-sum payment will increase your taxable income for the year, spreading out payments over time may not make a significant tax difference if your tax bracket remains the same. However, if your severance is substantial, consulting a tax professional to evaluate your specific situation can be worthwhile.

Can You Collect Unemployment If You Get Severance Pay?

The ability to receive unemployment benefits while collecting severance pay depends on your state’s specific laws. In some states, receiving severance pay may reduce or delay your unemployment benefits. Here’s an overview of how severance affects unemployment benefits in common scenarios:

- Lump-Sum Severance Payments: Some states allow you to receive unemployment benefits immediately after receiving a lump-sum payment. Others may require a delay before benefits can begin.

- Ongoing Severance Payments: If your severance pay is distributed in installments rather than as a single payment, it may impact unemployment benefits more significantly. In these cases, states often consider severance as a continuation of salary, which could disqualify you from unemployment benefits until the severance period ends.

Since state regulations vary, check with your state’s unemployment office to understand the rules specific to your area.

How Else Could Severance Affect Your Taxes?

Recognizing that severance pay is taxable can influence your overall tax planning and financial strategies. Severance pay can also impact other parts of your tax return and financial plans, such as:

1. Social Security and Medicare Taxes

Severance pay is subject to FICA taxes, meaning Social Security and Medicare will be deducted, just like with your regular paycheck. This can add a considerable amount to the overall tax withholding on severance.

2. Increased Tax Bracket

Receiving a large severance payout could push you into a higher tax bracket, resulting in a higher effective tax rate. A higher tax bracket means you’ll owe more on your severance payment and potentially on other income earned throughout the year.

3. Impact on Tax Credits or Deductions

If your severance pay increases your income significantly, it may affect eligibility for certain tax credits or deductions. For example, tax credits like the Earned Income Tax Credit (ETC) are income-based, and a large severance payment might make you ineligible for such credits, reducing your overall tax savings.

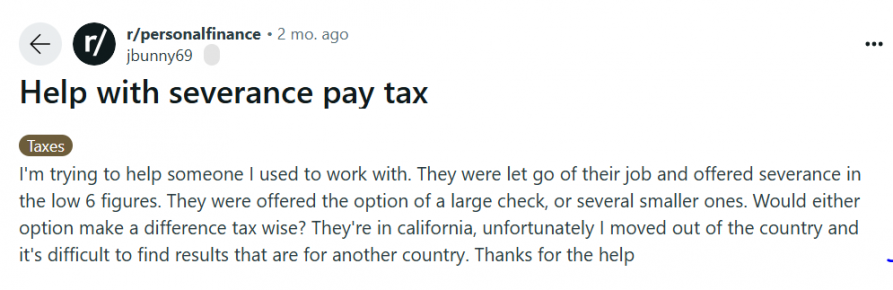

What People Are Saying On Forums

Navigating severance pay and its tax implications can be confusing, so looking at online discussions on forums like Reddit and Quora can provide real-world insights. Here’s a summary of two popular threads that may help:

Severance Payment As A Lump Sum Vs. Smaller Installments

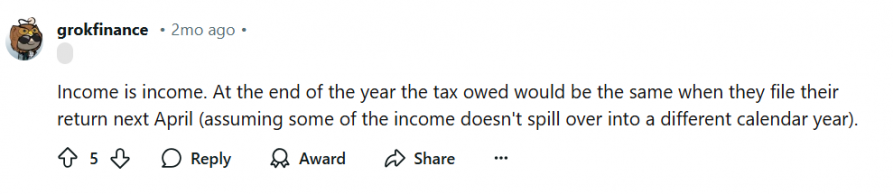

In one discussion, a user asked if receiving severance in one large check or in smaller, spread-out payments would impact taxes. Another user noted that, in general, income is income, and the IRS taxes it the same way, regardless of its distribution.

Here are some pros and cons to consider:

Pros Of A Lump Sum Payment:

- Immediate Access to Funds: With a lump sum, you’ll have access to the full severance amount right away, which can be helpful for managing expenses during a job search.

- Simplicity: Receiving the entire payment at once can make budgeting easier, as you won’t need to wait for smaller payments over time.

Cons Of A Lump Sum Payment:

- Higher Immediate Tax Impact: A single large payment may push you into a higher tax bracket, increasing the overall tax owed.

- Limited Options for Tax Minimization: It can be more challenging to spread out tax-saving strategies when receiving a one-time payment.

Pros Of Smaller Payments Over Time:

- Lower Tax Bracket Potential: Smaller payments over time may help you stay in a lower tax bracket, potentially reducing your tax liability each year.

- Income Stability: For those concerned about running out of funds too quickly, smaller installments can provide a steady income stream while job hunting.

Cons Of Smaller Payments Over Time:

- Delayed Access to Full Funds: Waiting for full severance may limit flexibility if immediate funds are needed.

- Complex Tax Planning: Managing tax implications over multiple payments can require more careful planning.

Choosing a lump sum or smaller payments depends on your financial needs, tax goals, and job prospects. Consulting with a tax professional can provide personalized guidance on the best option for you.

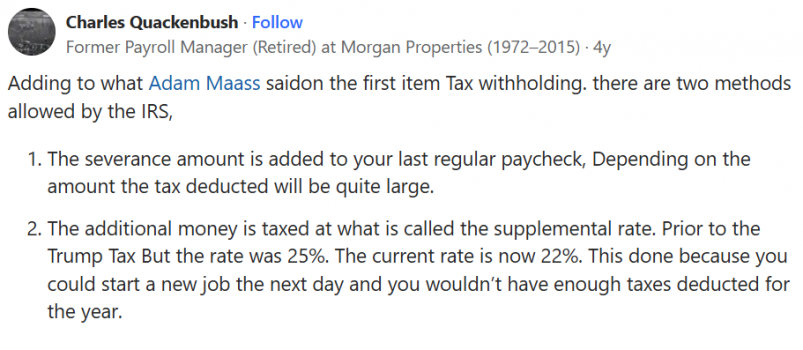

Is Severance Pay Taxed Differently Than Regular Pay?

One common question on Quora is whether severance pay is taxed differently from regular wages. One user pointed out that severance pay is taxed at what’s known as the supplemental rate—a flat rate currently set at 22%, which is different from the progressive rate applied to regular income. This rate was previously set at 25% before the Tax Cuts and Jobs Act, which lowered it to help individuals manage the tax impact on extra income like severance.

Do You Owe Tax Debt?

If you’re facing financial difficulties related to taxes, it’s essential to take proactive steps to resolve them. Being free of tax debt can improve your financial stability and reduce stress. The IRS can impose penalties and interest on unpaid taxes, and over time, these amounts can grow substantially.

If tax debt feels overwhelming, consider a reputable tax resolution company to help manage your liabilities. For help selecting a service, consult a trusted tax professional, research online, and compare companies' experience and client satisfaction. Here is a quick guide:

CuraDebt Reviews

At CuraDebt, our clients are at the heart of everything we do. Many clients share positive experiences, grateful for our support and expertise in resolving tax and debt issues. Our team is committed to finding solutions that fit each client’s unique needs, helping them regain financial control. CuraDebt’s commitment to quality and transparency has made us a experienced partner for people seeking tax and debt relief services.

If you’re facing tax debt, our free consultation offers a chance to discuss your situation and explore options with a professional. We’re here to guide you every step of the way, ensuring a solution that’s both manageable and effective.

Conclusion

Understanding severance tax implications is key to securing your financial future during a job transition. From minimizing taxes to exploring unemployment and consulting forums like CuraDebt, you have valuable resources to make informed decisions.

If tax debt is a concern, remember that CuraDebt is here to help. Our team of experts offers free consultation to assist you with tax relief solutions tailored to your needs. Taking control of your tax debt today can make all the difference for a brighter financial future.