Receiving a lawsuit notice for unpaid debt can be stressful and overwhelming. You might feel like there’s no way out, but the truth is, you have options. Many people assume they have to either pay the full amount or accept the consequences—but that’s not always the case. The right legal strategy can make a huge difference in how your case plays out.

In this guide, we’ll break down everything you need to know about debt lawsuits and how to fight back. From verifying whether the debt is even valid to challenging a creditor’s claims in court, you’ll learn practical steps to protect yourself and potentially get the case dismissed.

Understanding Debt Lawsuits

Getting sued over a debt can feel overwhelming, especially if you're not sure what the legal process looks like. But understanding what happens—step by step—can help you feel more in control and avoid missteps that could make things worse.

It Usually Starts with Collection Attempts

Before a lawsuit ever lands at your door, creditors (or the debt collectors working for them) typically try to collect the debt directly. You might receive phone calls, letters, or even settlement offers. At this stage, you still have the chance to resolve the issue without any legal involvement—through negotiation, a payment plan, or even a lump-sum settlement.

Ignoring these efforts doesn’t make them go away—and can lead to the next step: a formal lawsuit.

The Lawsuit Arrives: What to Expect

If those early attempts don’t work, the creditor might file a lawsuit in civil court. You’ll be served with two documents:

- A Summons, informing you that you’re being sued.

- A Complaint, which outlines how much the creditor says you owe and why they’re suing.

This is a key moment. If you don’t respond, the court may assume the claims are true—even if they’re not. The Consumer Financial Protection Bureau offers helpful guidance on how to respond effectively.

The Clock Is Ticking

You generally have 20 to 30 days to respond after being served, depending on your state. If you don’t, the creditor can ask the court for a default judgment, which could result in:

- Wage garnishment

- Frozen bank accounts

- Liens on property

That’s why responding is critical—even if you plan to negotiate or don’t think you owe the full amount. You may have legal defenses that can reduce or even eliminate what you owe.

Discovery & Documentation

After you respond, the case enters discovery—a stage where both parties exchange evidence. This is your chance to request proof that the creditor has the legal right to collect the debt. You can ask for:

- A signed agreement

- A record of account transfers (if a third-party collector is involved)

- An itemized breakdown of the debt

Creditors often don’t have all the required documentation, especially with older or transferred debts. If they can’t prove their case, you may be able to request a dismissal.

Check your state's civil court rules to understand your rights during discovery and to see if you can file a motion to dismiss based on insufficient evidence.

If the Case Goes to Court

If no settlement is reached, the case proceeds to court. Both sides will present their arguments, and a judge will decide the outcome. If the creditor fails to prove their claims, the case might be dismissed. If they succeed, a judgment will likely be entered against you—and that can include additional legal costs.

No matter what stage you're in, preparation and timely action matter. You don’t have to face it alone—and being informed puts the power back in your hands.

How to Get a Debt Lawsuit Dismissed

Now, let’s dive into the specific strategies that can help you get a debt lawsuit dismissed. Understanding your rights and taking the right steps can make all the difference in protecting yourself from a judgment. Here’s what you need to know:

1. Verify That The Debt Is Legitimate

Before doing anything else, make sure the debt is valid. Creditors are legally required to prove that you owe the amount they claim. You have the right to request debt validation within 30 days of receiving notice. Under the Fair Debt Collection Practices Act (FDCPA), they must provide:

- The original creditor’s name.

- A breakdown of the amount owed (including interest and fees).

- Proof that they have the legal right to collect the debt.

If they can’t provide this information, you may have grounds to challenge or dismiss the lawsuit.

2. Check if the Statute of Limitations Has Expired

Every state has a statute of limitations that limits how long creditors can sue for unpaid debts. If your debt is past this deadline, you can ask the court to dismiss the lawsuit.

💡 Tip: Even if the debt is old, making a payment or acknowledging it can restart the clock on the statute of limitations. Always check the status before taking action.

3. Challenge The Creditor’s Right To Sue (Lack Of Standing)

Debt is often sold multiple times between collection agencies, and sometimes, the current creditor doesn’t have the proper paperwork to prove they own your debt. If they can’t establish a clear chain of ownership, the lawsuit could be dismissed.

Ask the creditor to provide complete documentation showing how they obtained the debt from the original lender. If they fail to do so, you may have a strong defense.

4. Look For Errors In The Lawsuit

Mistakes happen, and errors in the creditor’s paperwork can work in your favor. Review all court documents carefully and check for:

- Incorrect debt amounts.

- Wrong account numbers.

- Misspelled names or outdated information.

Even small errors can weaken the creditor’s case and potentially get the lawsuit dismissed.

5. Negotiate A Settlement

If dismissal isn’t possible, you might be able to settle the debt for less than what you owe. Creditors often prefer partial payment over expensive court battles.

Pro Tip: Before negotiating, understand your financial limits and get any settlement agreement in writing to prevent future disputes.

6. Consider Bankruptcy (As A Last Resort)

If you’re drowning in debt and facing multiple lawsuits, bankruptcy may be an option. Chapter 7 bankruptcy can wipe out unsecured debts, while Chapter 13 allows for structured repayment.

📌 Important: Bankruptcy has long-term consequences, so it should only be considered after exploring other options.

What If You Can’t Get Your Debt Lawsuit Dismissed?

If dismissal isn’t an option, you still have ways to manage the lawsuit and reduce its impact. Ignoring it will only make things worse, so take action. You may be able to settle for less than what you owe, set up a payment plan, or challenge parts of the case to improve the outcome.

If a judgment is issued against you, learn how to protect your income and assets. Some funds, like Social Security, are shielded from creditors, and state laws may offer additional protections. If the debt feels impossible to manage, relief programs or bankruptcy could be options to explore.

No matter where you stand, you don’t have to face this alone.

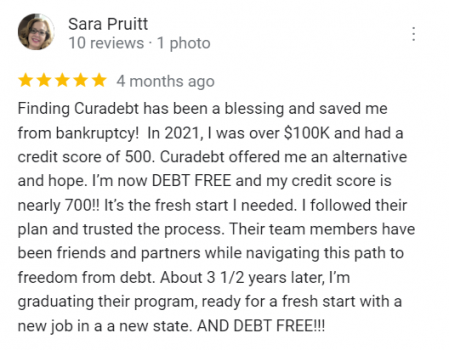

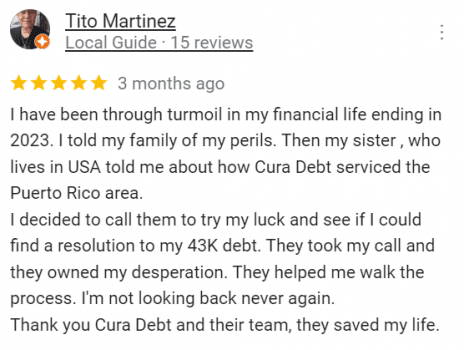

Real Stories From People Who Took Action

Facing debt can feel overwhelming, but taking that first step toward a solution makes all the difference. Many of our clients came to us feeling stuck, unsure of their options, and worried about their financial future. By exploring debt relief strategies—whether through settlement, negotiation, or other means—they found a path forward and regained control of their finances.

From reducing overwhelming balances to avoiding aggressive collection tactics, our clients have seen real results. But don’t just take our word for it—see what they have to say about their experiences:

Taking Control of Your Financial Future

Dealing with a debt lawsuit can feel like an uphill battle, but you don’t have to face it alone. Whether you’re fighting to get the case dismissed, negotiating a settlement, or figuring out your next steps, what matters most is taking action. Ignoring the problem won’t make it go away, but making informed decisions can put you back in control.

We understand how stressful and overwhelming this process can be. That’s why we’re here to help. Our team has guided countless people through difficult financial situations, offering real solutions that work. If you’re unsure about your options or need help navigating your lawsuit, we’re ready to assist. Contact us today for a free consultation, and let’s find the right path forward together.