Dealing with debt is stressful enough—then comes tax season, and suddenly, you’re hit with IRS Form 1099-C. If a creditor cancels a debt of $600 or more, they’re required to send you this form, and it’s also reported to the IRS. That canceled debt might now be considered taxable income, which can come as an unpleasant surprise.

But here’s the thing: just because you receive a 1099-C doesn’t always mean you owe taxes on the forgiven debt. There are exclusions and ways to manage this situation—so don’t panic. Let’s break it all down in a way that actually makes sense, so you can understand what to do next and how to protect yourself from unnecessary tax burdens.

What is IRS Form 1099-C?

Simply put, IRS Form 1099-C is the way creditors tell both you and the IRS that they have forgiven or canceled your debt. This applies to debts like credit cards, personal loans, or medical bills.

But why does this matter? Because in the eyes of the IRS, canceled debt is often treated as taxable income. That means you could end up owing taxes on money you never actually received in cash—just debt that disappeared.

However, not all canceled debts are taxable. Some exceptions exist, such as:

- If the debt was discharged in bankruptcy.

- If you were insolvent (your total debts were greater than your total assets) at the time.

- If the debt was related to certain student loan forgiveness programs.

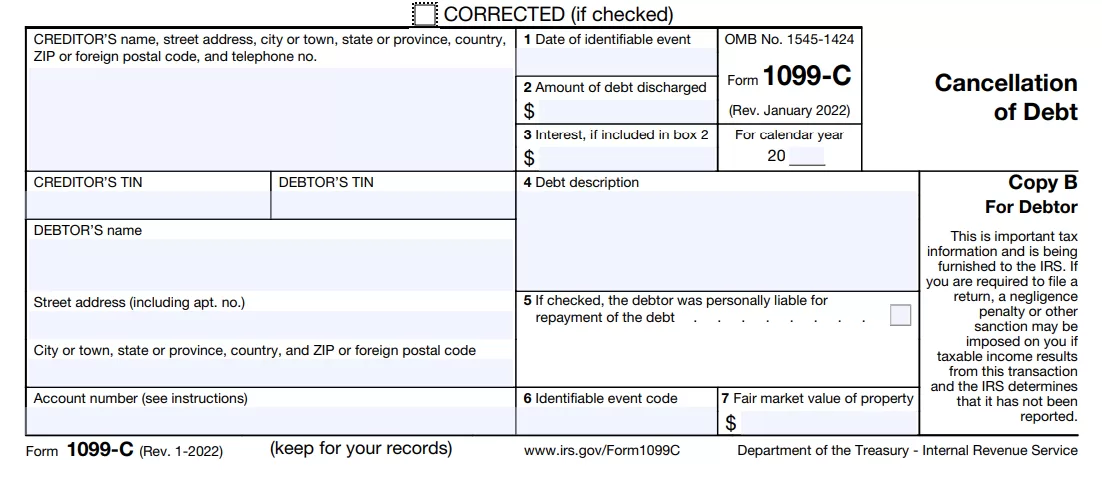

Example Of IRS Form 1099-C

Seeing an actual 1099-C form can help you better understand what to look for. This form includes details like the amount of canceled debt, the creditor’s information, and the date of cancellation. Below is an example of how it looks, so you can recognize key sections when reviewing your own. Always double-check the information for accuracy, as errors can impact your tax situation.

Common Situations That Trigger a 1099-C

Here are some of the most common scenarios where this happens:

- Settled Credit Card Debt – If you negotiated with your credit card company and paid less than what you originally owed, the forgiven balance may be reported as taxable income.

- Mortgage Debt Forgiveness – Short sales, foreclosures, and loan modifications can lead to mortgage debt cancellation, which lenders typically report to the IRS.

- Student Loan Forgiveness – While some student loan forgiveness programs are tax-exempt, others may require you to report the discharged amount as income. Always check the tax implications of your specific program.

- Auto or Personal Loan Cancellations – If your car was repossessed or you settled a personal loan for less than the full balance, the remaining amount might be considered canceled debt and reported to the IRS.

Each of these situations has potential tax consequences, but there may be exclusions or ways to reduce the impact. Understanding your options can help you avoid unnecessary tax burdens.

What To Do If You Receive a 1099-C

Receiving a 1099-C means a creditor has officially canceled a debt, but that doesn’t always mean you owe taxes on it. Here’s how to handle it properly and avoid unnecessary costs:

- Verify the Details: Creditors make mistakes. Double-check that the canceled debt amount is correct and that the lender’s information matches your records. If anything looks off, contact the creditor immediately to request a correction.

- See If You Qualify for an Exclusion: Not all canceled debt is taxable. If you were insolvent at the time of cancellation or went through bankruptcy, you might be able to exclude the forgiven amount by filing IRS Form 982. This can help you avoid paying taxes on debt you were never able to afford in the first place.

- Report It Properly: If you don’t qualify for an exclusion, you’ll need to include the forgiven debt as part of your taxable income. Ignoring it could lead to IRS penalties or an unexpected tax bill later.

- Get Expert Guidance: Tax laws around canceled debt can be confusing. If you’re unsure about how to proceed, working with a tax relief specialist can help you minimize what you owe and avoid costly mistakes.

Using IRS Form 982 with Form 1099-C

IRS Form 982 provides important provisions for reducing taxable income from canceled debt under specific circumstances:

- Qualifying Exclusions: Taxpayers can exclude canceled debt from income by meeting criteria like bankruptcy or insolvency during cancellation. They can also exclude canceled debt if it is qualified principal residence indebtedness forgiven before January 1, 2021.

- Step-by-Step Filing: Detailed instructions on how to complete and file Form 982 to claim exclusions from canceled debt. Taxpayers should ensure all required information is provided and supporting documentation is attached as necessary.

- Documentation Requirements: Taxpayers must provide adequate documentation to substantiate claims for exclusions under Form 982. This may include bankruptcy filings, insolvency worksheets, or other supporting evidence of financial condition at the time of debt cancellation.

Understanding IRS Form 1099-C and Form 982 helps manage canceled debt, minimizing tax liabilities effectively for taxpayers.

IRS Form 1099-C Statute of Limitations:

The IRS form 1099-C statute of limitations sets the timeframe during which the IRS can assess additional taxes or the taxpayer can amend returns related to canceled debt income. Typically, this statute extends for three years from the due date of the tax return with reported canceled debt income. It’s crucial for taxpayers to be aware of these limitations to avoid potential penalties or misunderstandings regarding their tax liabilities.

Understanding the IRS form 1099-C statute of limitations ensures that taxpayers can manage their tax obligations effectively, preventing surprises and penalties down the line. Keep precise records of canceled debts and tax filings to meet IRS requirements within the statute of limitations.

IRS Form 1099-C Instructions

The IRS provides detailed instructions for completing Form 1099-C, including:

- Required Information: Taxpayers must accurately report the amount of canceled debt and provide essential details such as the debtor’s identifying information and the creditor’s information.

- Deadline and Submission: Form 1099-C must be issued to debtors by January 31st following the year of debt cancellation. It should be filed with the IRS by February 28th or March 31st (if filed electronically) with the tax return.

- Corrections and Amendments: Procedures for correcting errors on Form 1099-C or amending tax returns if necessary. Taxpayers should promptly address any inaccuracies to avoid potential penalties or delays in processing.

Conclusion

Dealing with a 1099-C form can feel overwhelming, but understanding your options puts you back in control. Whether your canceled debt leads to a tax bill or qualifies for an exclusion, knowing how to handle it can make all the difference.

We’ve covered what IRS Form 1099-C means, how it affects your taxes, and what steps you can take to minimize the impact. The key is not to ignore it—double-check the details, explore potential exclusions, and take action before tax season catches up with you.

If you’re unsure about the next step or want to reduce your tax burden, you don’t have to figure it out alone. The CuraDebt team specializes in helping people navigate IRS tax debt, and we’re here to help you find the right solution for your situation. Schedule a free consultation today and let’s work together toward financial relief.