When you’re navigating the world of business financing, the term “personal guarantee” is bound to come up. While it might sound like just another step in the loan approval process, a personal guarantee is a serious commitment that can impact not only your business but also your personal financial well-being.

Before signing on the dotted line, it’s crucial to understand what a personal guarantee entails, how it works, and the risks involved. This article will delve into the essentials of personal guarantees, their types, alternatives, and what to consider before making a decision. Along the way, we’ll show you how CuraDebt’s free consultation can help if your business is already dealing with debt.

Let’s break it all down to ensure you’re making informed decisions for your business and your future.

What Is A Personal Guarantee?

A personal guarantee is a legal commitment where an individual promises to repay a business loan or debt if the business cannot meet its financial obligations. Essentially, it shifts the lender’s risk from the business to you, the guarantor, by allowing them to pursue your personal assets if the business defaults.

For example, if you own a small business and take out a loan with a personal guarantee, you’re not just putting your business’s financial stability on the line but also your personal savings, real estate, or other assets.

This arrangement is commonly used by lenders to provide loans to startups, small businesses, or companies with limited credit history, as it offers them additional security.

Is your business in debt? CuraDebt is here for you.

How Personal Guarantees Work

When you sign a personal guarantee, you essentially act as a co-signer for your business. Here’s how the process generally works:

1. Loan Application

Lenders evaluate your business’s financial health, including credit scores, cash flow, and assets. If they determine that the business alone isn’t a strong enough candidate, they may require a personal guarantee to approve the loan.

2. Signing The Agreement

The personal guarantee agreement specifies your liability and outlines the terms under which the lender can pursue your personal assets. It’s essential to read and understand every clause in this document.

3. Debt Repayment Or Default

As long as your business repays the loan as agreed, your personal guarantee won’t come into play. However, if the business defaults, the lender can bypass the business entirely and hold you personally accountable for the debt.

Types Of Personal Guarantees

Not all personal guarantees are created equal. Here are the main types:

1. Unlimited Personal Guarantee

Under this agreement, the guarantor is fully liable for the entire debt amount, including any fees, interest, or legal costs. This type exposes you to the highest level of financial risk.

2. Limited Personal Guarantee

A limited guarantee caps your liability to a specific amount, which is often proportional to your ownership stake in the business. This arrangement is common in partnerships or businesses with multiple owners.

3. Joint And Several Guarantees

In this case, multiple guarantors share responsibility for the debt. Creditors can pursue one or all guarantors to recover the total amount.

4. Specific Guarantee

This type of guarantee is limited to a single loan or transaction, rather than applying to all the business’s debts.

Alternatives To A Personal Guarantee

If you’re uncomfortable signing a personal guarantee, there are other options to consider:

1. Business Collateral

Offer physical assets like equipment, inventory, or real estate as collateral. This provides lenders with security without tying your personal finances to the loan.

2. Equity Financing

Consider selling a stake in your business to investors rather than taking on debt. While this approach involves sharing ownership, it eliminates the risk of personal liability associated with a guarantee.

3. Government Loans

Explore programs like SBA (Small Business Administration) loans or other government-backed financing options. These loans often come with more favorable terms and do not require personal guarantees, depending on the specific program.

4. If You Already Have Debt, CuraDebt Can Help

If your business is already carrying debt, and you’re struggling to manage repayments, CuraDebt is here to assist you. Our team specializes in creating personalized strategies to help businesses reduce debt and regain financial stability.

With over 25 years of experience, we’ve helped countless businesses navigate debt challenges. Contact us for a free consultation to explore how we can help you achieve relief and get your business back on track.

By considering these alternatives and seeking professional support, you can secure financing while protecting your personal assets and ensuring your business’s long-term success.

Exploring Forums And Communities

Platforms like Reddit and Quora can provide firsthand accounts and advice from people who have dealt with personal guarantees. These communities often share real-life experiences, tips, and insights that can help you better understand the potential challenges and considerations.

While these forums can be a helpful starting point, it’s essential to cross-reference any advice with guidance from financial professionals to ensure you’re making sound and informed decisions. Always prioritize understanding the fine print of any agreement you’re signing.

Does Your Business Have Debt? CuraDebt Can Help

Managing business debt can feel overwhelming, especially when personal guarantees are involved. That’s where CuraDebt comes in.

Why CuraDebt?

- Expert Guidance: We’ve been helping business owners like you navigate debt challenges for over 25 years.

- Personalized Solutions: Every business is unique, and we tailor our approach to suit your specific needs.

- Free Consultation: Our no-obligation consultation lets you explore your options and take the first step toward financial relief.

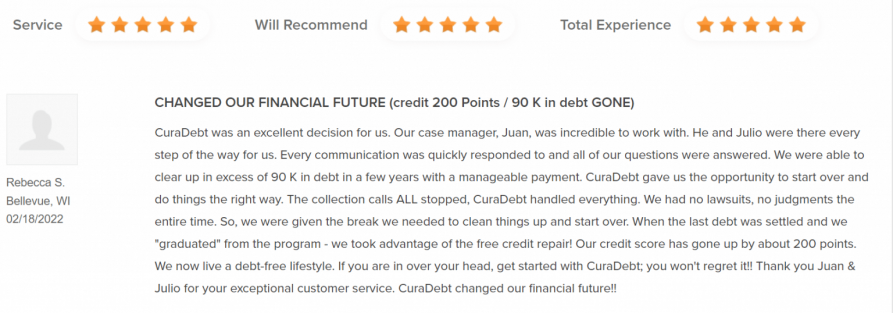

Imagine being free from the weight of your business debt. Call us today for a free consultation and see how we can help you regain control of your financial future. This is what some of those we have helped say about us.

Conclusion

Personal guarantees are a double-edged sword. While they can help your business secure the funding it needs, they also expose you to significant financial risks. By understanding their terms, exploring alternatives, and seeking professional advice, you can make informed decisions that protect your future.

If your business is dealing with debt, CuraDebt is here to help. With a proven track record and personalized solutions, we’re ready to guide you toward financial freedom. Contact us today for your free consultation and start your journey to a debt-free future.